Making a core banking software switch is no small task. But for many banks and credit unions, the time has come to do so, or at least consider the possibility. As American Banker explained, “Some banks still use core software purchased 30 or more years ago, and have layered on top of it ‘ancillary’ products such as online banking and mobile banking software, creating a complex IT environment that is hard to manage and upgrade to launch new products and comply with emerging regulations.”

This outdated technology is quickly becoming cumbersome for banks and credit unions that want to compete in the digital age. As the Financial Brand aptly stated, “it’s time to bite the bullet and get serious about a core conversion.”

Because a core conversion is a massive undertaking, in both time and money, many banks and credit unions are hesitant. However, with precise planning and foresight, you will be able to not only choose the best core software for your bank or CU, but ensure that the implementation process runs as smoothly as possible.

Choosing the Best Core Banking Software

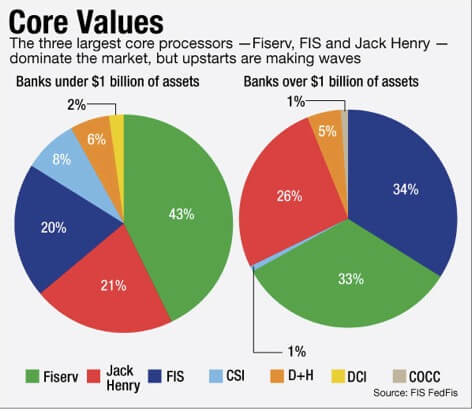

Today, there are four primary core banking providers, FIS, Fiserv, Jack Henry and D+H, that have managed to eat up 96 percent of the market share (90 percent for banks under $1 billion in assets and 98 percent for banks over $1 billion in assets). But there are also some strong players rounding out the remaining 4 percent.

| Top Core Banking Software Vendors | Top Core Credit Union Software Vendors |

| Fiserv | Fiserv |

| Jack Henry | Symitar |

| FIS | FIS |

| CSI | Harland |

| D+H | Share One, Inc. |

| DCI | COCC |

| COCC | CU Prodigy |

| Bankway by IBM | CUnify |

| Corelation |

Deciding on a core software is the first key task for banks and credit unions looking to make the switch. But the decision is not one to be taken lightly, as pointed out by Forbes “Core technologies are evolving into highly agile architectures, and the implications for making the wrong decision will be lasting — and could put banks at competitive risk.”

To help your bank and credit union make the best use of your resources, Gartner identified the eight key criteria that have the most impact on core banking system decisions:

- Functionality

- Flexibility

- Cost

- Viability

- Operational Performance

- Program Management

- Partner Management

- Customer References

Ensuring a Smooth Core Software Implementation

Consider componentization if you are a larger bank.

A decade or more ago, a core implementation would take 5-10 years. Today, implementation is much faster, with smaller banks typically able to convert to a new system within 12 months. For the larger banks and credit unions, however, the time frame is a bit longer and the complexity of the job is that much greater. To help limit disruptions to the business and speed up the time to launch, more core software providers have offered banks and credit unions the ability to change out their core software piece by piece, in a tactic known as “componentization.” If you are a larger bank or credit union, you may want to inquire about componentization.

Choose the right implementation partner.

Deloitte, in a paper on core banking transformation, likened a core banking conversion to open heart surgery, noting the challenges and risks involved with both. Due to the complexity of a core switch, engaging an implementation partner that can help guide your bank or credit union along the transformation journey is paramount. Deloitte offered advice on how to choose a systems integrator, noting that they should be able to prove their qualifications and capabilities in the following areas:

- Maintaining the benefits case

- Breadth of experience encompassing business, people, and technology

- Business and solution architecture

- Business operations and change readiness

- Software package expertise

- Data migration

- Integration

- Vendor management

- Project governance and delivery

- Quality assurance and management

- Capacity building and knowledge transfer

Have a plan for disruption to normal business.

Any change within a bank or credit union will affect business as usual. But a core change brings with it the potential for the type of disruption caused by a large event, such as a merger or acquisition. With the right technology in place, however, you can mitigate the negative effects that this large systems change can have. Namely, you can ensure that your customers and members are able to access all the information they need on your digital channels with ease, thereby relieving the call center, which often becomes overrun in times of change.

Clean out the old core system.

Just like moving to a new house, moving to a new core system offers you the perfect opportunity to clean up and throw out anything that no longer serves you. Inventory your system with the goal of removing any obsolete features and identifying legacy products that are no longer worth maintaining.

Technology is evolving and customer and member demands are evolving with them. For banks and credit unions, this is resulting in an urgent need to re-evaluate current legacy systems, especially the core banking software that is the powerhouse behind most financial institutions.

At Engageware, we help banks and credit unions manage large changes through our SaaS- based software. So, if you’re planning on moving forward with a core software change, contact us to learn how we can help ensure it is a smooth transition.